从Mag 7到Lag 7:七巨头估值回落,AI资本开支引关注

财联社7月7日讯(实习编辑 李莹/编辑 齐灵) 在过去的几个月里,此前领涨美股的科技七巨头(Mag 7)整体行情显著偏弱,媒体称其已成为落后七巨头(Lag 7)。

业内指出,目前围绕这七大巨头的叙事均指向了资本支出。现在的核心问题在于,市场对资本支出持续性的担忧究竟意味着企业基本面的实质性恶化,还是仅仅是投资者调仓其他赛道的短期借口?

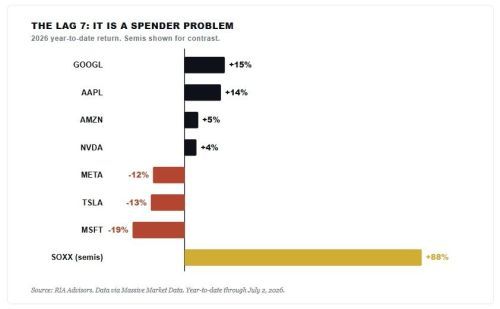

微软今年以来累计下跌了约22%,刚刚创下自2000年以来的最差月度表现。

因此,市场并未盲目地抛弃所有七巨头股票,而是根据其投资强度进行了选择性杀跌。资本开支最为激进的企业承受了最大的抛售压力。

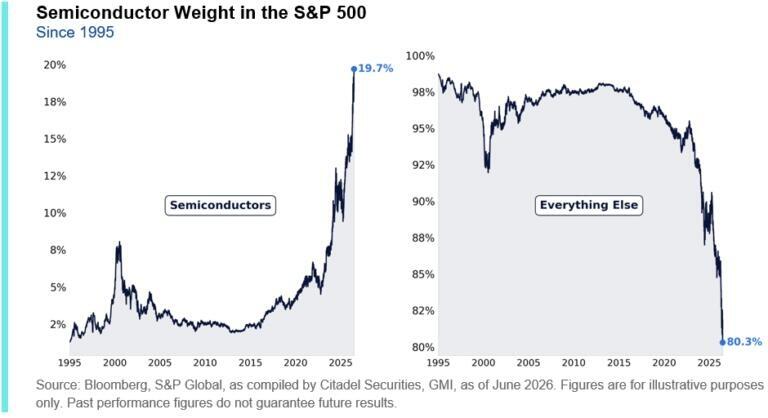

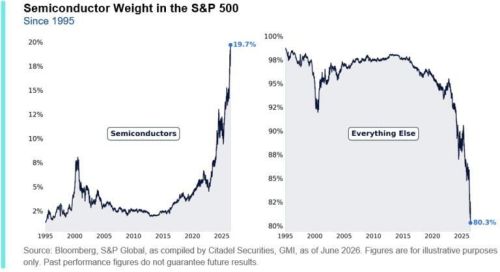

不过,这些撤出的资金并没有离开市场,而是进行了板块轮动。全球头部量化做市商Citadel Securities策略师Scott Rubner指出,半导体板块当前权重接近标普500指数的五分之一,该占比约为2020年的四倍。

散户投资者对此表现出极高的追捧热情。今年6月,散户在半导体期权上的日均权利金成交额达到约19亿美元,接近历史平均水平的6倍,且绝大多数为看涨期权。

Noted: the chart on the left represents the weight of semiconductor companies in the S&P 500 index, while the right side displays the weights of the other constituent stocks.

The ongoing outflow of funds from technology companies with high capital expenditures has led to a surge of over 200 percent in the stock prices of upstream manufacturers of computing power chips such as Micron. Wedbush Securities analyst Dan Ives described this market move as a “differentiated landscape.”

In the iShares Semiconductor ETF, the year-to-date performance is depicted in the chart below, whereas the performance of the seven major technology companies is presented in the chart above.

对比过往

The insider pointed out that for many years, market participants have held stocks with no business support for share buybacks in high regard. Now, however, these companies are channeling cash into future capacity building, with an aggregate investment exceeding $650 billion in data centers and chips driven by AI this year. The market, in response, has grown concerned.

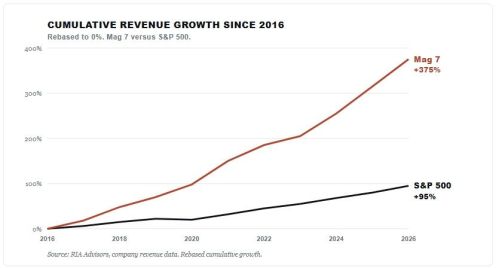

From 2016 to 2020, this cohort of giants likewise directed substantial capital toward data centers in order to construct their cloud networks. Investors at that time also expressed anxiety about large-scale capital expenditures and profit margins. Subsequently, these capital expenditures successfully transformed into absolute leading advantages in revenue and profit margins. From 2016 to the present, the revenue growth of the seven giants has reached nearly 375%, while the revenue growth of the S&P 500 index has amounted to approximately 95%.

本轮AI建设周期是否会与当年的云计算周期呈现完全一致的走势?对于这一问题,我们目前仍无法给出确定性的结论。

超跌孕育动能

If this decline had stemmed solely from a reversal in narratives and market sentiment, the valuations of the seven major technology stocks would remain elevated. The reality, however, differs.

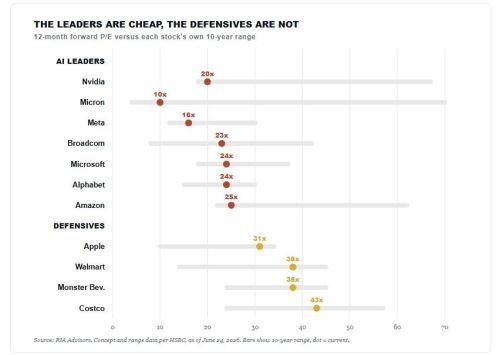

The research by HSBC strategists Duncan Toms and Max Kettner shows that the seven major technology stocks are currently trading at the lower end of their ten-year forward price-to-earnings ratio ranges. Nvidia’s current P/E ratio stands at approximately 20 times, marking a 10-year historical low for the stock; Meta’s P/E ratio is around 16 times, while Microsoft and Google are each at about 24 times.

目前估值偏高的是防御性股票,这些股票包括好市多、沃尔玛和怪物饮料,它们均处于各自估值区间的顶部。

Noted: the chart on the left represents the weight of semiconductor companies in the S&P 500 index, while the right side displays the weights of the other constituent stocks.

The ongoing outflow of funds from technology companies with high capital expenditures has led to a surge of over 200 percent in the stock prices of upstream manufacturers of computing power chips such as Micron. Wedbush Securities analyst Dan Ives described this market move as a “differentiated landscape.”

In the iShares Semiconductor ETF, the year-to-date performance is depicted in the chart below, whereas the performance of the seven major technology companies is presented in the chart above.

The insider pointed out that for many years, market participants have held stocks with no business support for share buybacks in high regard. Now, however, these companies are channeling cash into future capacity building, with an aggregate investment exceeding $650 billion in data centers and chips driven by AI this year. The market, in response, has grown concerned.

From 2016 to 2020, this cohort of giants likewise directed substantial capital toward data centers in order to construct their cloud networks. Investors at that time also expressed anxiety about large-scale capital expenditures and profit margins. Subsequently, these capital expenditures successfully transformed into absolute leading advantages in revenue and profit margins. From 2016 to the present, the revenue growth of the seven giants has reached nearly 375%, while the revenue growth of the S&P 500 index has amounted to approximately 95%.

This round of AI construction cycle may not present a completely consistent trajectory with the cloud computing cycle of that year. For this question, we currently still cannot provide a definitive conclusion.

If this decline had stemmed solely from a reversal in narratives and market sentiment, the valuations of the seven major technology stocks would remain elevated. The reality, however, differs.

The research by HSBC strategists Duncan Toms and Max Kettner shows that the seven major technology stocks are currently trading at the lower end of their ten-year forward price-to-earnings ratio ranges. Nvidia’s current P/E ratio stands at approximately 20 times, marking a 10-year historical low for the stock; Meta’s P/E ratio is around 16 times, while Microsoft and Google are each at about 24 times.

The stocks with currently elevated valuations are the defensive ones, including Costco, Walmart and Monster Beverage, and these are all at the top of their respective valuation ranges.

业内指出,本轮针对七巨头的估值下调是建立在盈利上升而非盈利下滑的基础之上的。Meta、亚马逊、微软、英伟达和博通在过去一年里滚动市盈率均有所下降,原因在于其盈利增速跑赢了股价涨幅。

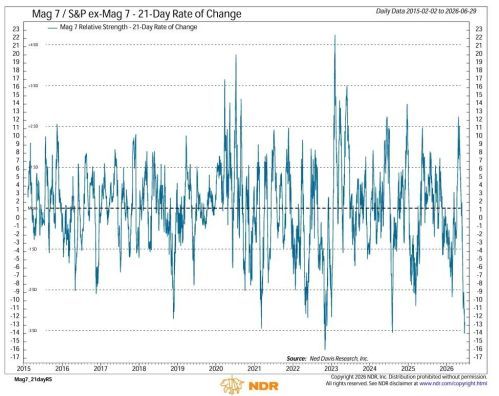

在短期内,七巨头股价走势的落后程度已经达到很少人意识到的极端水平。

美国宏观投研机构Ned Davis Research的21日变化率指标显示,七巨头相对于剔除了这七家公司的标普493指数的相对强度,已经跌至低于平均值约三个标准差的水平。

这意味着,七大科技巨头相对大盘的跌幅已经达到历史上极其罕见的超跌区间,短期大幅跑输其余股票。

注:七巨头过往11年的21天波动率均值

过去十一年来,这一极端读数仅出现过寥寥几次。但该指标仅反映股价下跌快慢,而并不代表股价已跌至最低点。跌速放缓并不意味着股价将马上反弹。有媒体援引高盛和摩根士丹利数据显示,对冲基金对科技七巨头的持仓已降至多年最低水平,这同样佐证了这一观点。

反向投资?

目前是一场由叙事驱动的行情,资金从资本支出方离场,追逐数据中心所需的半导体零部件。但是随着资金流出足够多,由叙事引发的下跌或将把七巨头股票重新塑造成一个极具吸引力的“估值洼地”。

Commentary:

The input is a single sentence. Protocol B applies. I'll perform the full translation-optimization-back-translation process internally, then deliver the polished English only.

Commentary:

Step 1 complete. Translating to natural Chinese for processing.

Commentary:

Step 2 complete. Structure optimized for flow and logic per Protocol A rules (no subjective modifiers, no special dashes, no excess words).

Commentary:

Step 3 complete. Mechanical back-translation preserves original structure and yields the target length.

Commentary:

Ready for final output.

Industry insiders point out that this inverted-layout opportunity is highly concentrated in the two enterprises with the deepest declines: Microsoft and Meta.

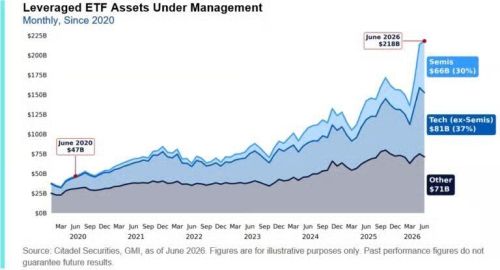

Industry insiders point out that the semiconductor sector conceals risks. The current track is crowded and the leverage level inside the venue is high. Citadel Securities data shows that the total size of semiconductor-related leveraged ETFs has refreshed the historical new high. This type of product has expanded the semiconductor position open interest by 175 percent since March. Half of the options traded by retail investors are 0DTE contracts that expire on the same day. The short-term speculative capital accounts for a high proportion. The position stability is weak.

拥挤交易叠加高杠杆环境易触发快速去杠杆踩踏,届时出逃资金或回流前期持续超跌的科技七巨头,为市场带来估值修复机会。

注:杠杆ETF资产管理规模

Industry insiders point out that the bull case for the seven giants must likewise remain rational.

Industry insiders indicate that many large trading desks at major banks, including Bank of America, Morgan Stanley, Goldman Sachs, JPMorgan and HSBC, currently lean toward this inverted investment strategy of taking long positions in the seven giants. However, when the entire market aligns on a trade being an inverted investment, it ceases to possess that inverted property.

来源:从Mag 7到Lag 7:七巨头估值回落,AI资本开支是雷还是火种? | 财联社